CBDC and stablecoins, between monetary sovereignty and geopolitics

The digital transformation of payment methods is shaping the contours of monetary sovereignty and geopolitics. In China, the e-CNY has moved beyond the experimental stage to become a daily reality. In Europe, the European Central Bank is refining a digital euro project aimed at preserving the continent's financial autonomy in the face of the growing dominance of dollar-backed stablecoins. In Switzerland, the National Bank is taking cautious steps with its Project Helvetia, exploring a wholesale central bank digital currency to modernise the Swiss financial infrastructure without disrupting the existing equilibrium.

Before governments developed digital currencies, the private sector had already taken steps in this direction. With USD 250 billion in stablecoins, privately issued digital currencies linked to national currencies have grown rapidly. According to a July 2025 McKinsey report (The stable doors open: How tokenised cash enables next-gen payment), daily dollar payments amount to between USD 5,000 and 7,000 billion versus only USD 20 to 30 billion for stablecoins. Although a drop in the ocean, at the current growth rate, transaction volumes could surpass this figure within a decade, the report suggests.

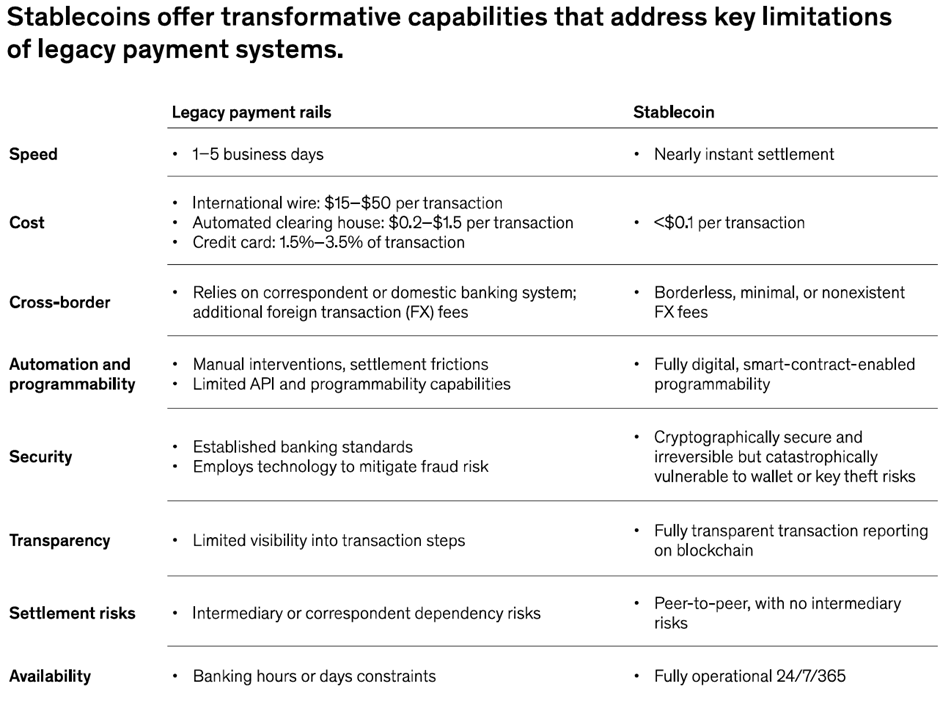

This rapid growth seems plausible when considering the advantages offered by this mode of payment compared to current systems: speed, cost, transparency, availability, inclusion. Overall, the table below, borrowed from McKinsey's study, is unequivocal; among the eight criteria, seven clearly favour stablecoins. The eighth, security, is a double-edged sword, as it encompasses two concepts. Cryptographic security is excellent; the issue is that once a transaction is completed, it cannot be reversed — this is the concept of irreversibility. In case of an error, irreversibility is problematic, but it also fosters trust.

Of course, stablecoins carry risks and require better regulation to prevent incidents like Terra-Luna and its stablecoin UST, whose value was eradicated in a matter of hours. Algorithmic stablecoins like UST are banned in most jurisdictions, favouring "traditional" stablecoins whose value is backed by deposits of equivalent fiat currency. Similarly, the use of digital currencies offers a significant degree of anonymity, with risks of terrorism financing and money laundering. Identifying the economic beneficiary has become common practice in finance and is increasingly applied to stablecoins.

Monetary sovereignty and financial geopolitics

While protecting users is essential, the regulation of stablecoins also has a strategic dimension — between monetary sovereignty and financial geopolitics. It is no surprise that their regulation is explicit, whereas the regulation of native cryptocurrencies like Bitcoin or Ether remains incomplete or even non-existent. The July 2025 GENIUS Act, signed by President Trump — pro-cryptocurrency — regulates only stablecoins. This highlights the strategic importance of stablecoins in terms of monetary sovereignty and geopolitical influence, compared to other cryptocurrencies.

Different regulations and the design of CBDCs reflect each country's strategic and political vision. Should access to central banks be direct for individuals, risking the fragility of commercial banks, or should a mediated model be maintained, where banks continue to serve as deposit collectors and credit distributors? Should the focus be on a wholesale version for financial institutions — facilitating settlement of tokenised securities — or on a retail version aimed at the general public for everyday payments? Is the priority to rapidly develop stablecoins and create links with central banks to ensure systemic stability, or to strengthen the current system and risk being overtaken by another government?

One thing is sure: in the face of the digital Silk Road that the e-CNY hints at, and the rapid growth of stablecoin usage, the current slow and costly international payment system must be modernised. It's not merely a matter of technological catch-up; it's also about financial hegemony.

Every choice shifts the balance of power between states, banks, and new private actors.

In this evolving landscape, stablecoins occupy a unique position. First, the complete dominance of the dollar consolidates its power in the digital realm and reinforces its hegemony. Second, behind each dollar stablecoin, there is debt issued by the US government. The creation mechanism of stablecoins is like that of money market funds. Therefore, promoting stablecoin use supports US debt through ongoing, large-scale purchases of Treasury bonds.

The e-CNY explicitly aims to reduce Asian dependence on the dollar and strengthen China's regional influence. The digital euro project seeks to safeguard European autonomy in international payments. Meanwhile, the United States is cautious that the global use of the dollar — now including stablecoins — remains unchallenged. Currency, in this context, becomes a tool of strategic competition as much as an instrument for economic settlement.

It all boils down to a tension between prudence and audacity. States aim to promote innovation without losing control, integrate stablecoins without ceding sovereignty, modernise monetary policy without undermining the banking sector, and project their currencies internationally by proposing a new payments system without destroying established systems.

The decisions made today will determine whether the currency of tomorrow remains a tool for stability or becomes a source of division. One thing is certain: in this new digital order, native cryptocurrencies may flourish as assets, but the monetary function will remain fiercely safeguarded by states. Regulated CBDCs and stablecoins are not merely technical tools; they are the key to the economic sovereignty of the 21st century.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications