How the AI Bubble Was Born from the Ruins of Wall Street

The artificial intelligence bubble is huge, worth around $46 trillion — roughly 1.5 times the size of the U.S. economy. It dwarfs the dot-com mania of the early 2000s. Yet this bubble did not emerge from Silicon Valley's labs or OpenAI's servers, but from the rubble of Wall Street after the 2008 financial crisis. Despite its name, the AI bubble has surprisingly little to do with AI itself.

How did it form? Why has it lasted so long? What keeps it inflated? And what might finally make it burst?

From crisis to euphoria

The roots of today's speculative excess lie in the extraordinary economic and financial policies rolled out to save the system after the Global Financial Crisis.

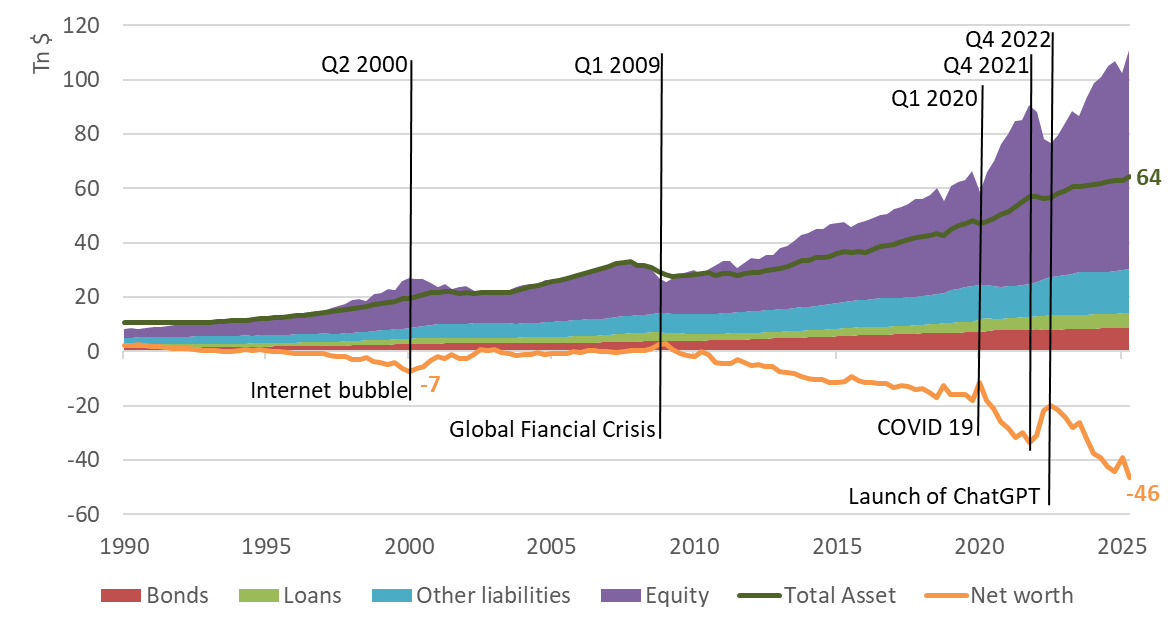

In early 2009, the S&P 500 hit its post-crisis low, down more than 55%. Sixteen years later, the index has risen tenfold. Market valuations have floated far above fundamentals — as shown by the orange line in Figure 1 — creating an estimated $46 trillion imbalance, about 1½ times U.S. nominal GDP.

Measuring the madness

Before dissecting the bubble's anatomy, consider Figure 1. It charts the main balance-sheet items of the U.S. non-financial corporate sector.

- Dark green line: total assets, now about $64 trillion.

- Coloured areas: the liabilities — red for bonds, light green for loans, blue for other liabilities (creditors, pensions, etc.), and purple for equity.

- Orange line: net worth, the gap between assets and liabilities, our yardstick for the speculative excess — roughly $46 trillion.

Net worth matters because the Flow of Funds data values assets and liabilities at market prices, not historical cost. The gap between the two, therefore, captures the market imbalance between what firms are worth and how they are financed.

In these accounts, the difference is called "net worth", not "equity", because liabilities already include the market value of shares. A positive net worth suggests undervaluation; a negative one signals overvaluation — the hallmark of a bubble.

The long inflation

The bubble began forming as soon as markets stabilised in 2009.

In the first episode (Q1 2009–Q1 2020), the mix of rock-bottom interest rates, meagre bond yields and fears over European debt gave rise to the famous acronym TINA — "There Is No Alternative." That mantra drove a tidal wave of capital into equities, pushing corporate net worth below zero and inflating the bubble.

The second episode (Q1 2020–Q4 2021) coincided with the pandemic, when the bubble swelled at record speed. The 2009–2020 expansion was already the longest in U.S. history; the COVID recession, by contrast, was the shortest ever — barely two months — because it unleashed the most significant monetary and fiscal stimulus on record.

Though life froze during lockdowns, the economy merely sneezed. The "triple therapy" — zero rates, massive liquidity and fiscal firepower — worked wonders once again. Economic variables rebounded swiftly, and the bubble grew even fatter.

In the third episode (Q4 2021–Q4 2022), dependence on that triple therapy became clear. When the pandemic ended, fiscal stimulus remained huge and liquidity creation continued — this time through money-market funds rather than the Fed — converting U.S. government debt into the liquid fuel that kept the bubble alive.

Only one major change occurred: the Federal Reserve's rate hikes, from 0% to 5.25% between March 2022 and July 2023. That tightening deflated the bubble by roughly a third — but did not pop it.

Episode IV: A New Hope

The launch of ChatGPT in Q4 2022 marked the start of a new phase. With AI came a fresh narrative — the promise of a revolution even more transformative than the internet a generation earlier. As in the late 1990s, the dream of a new technological era — and the fear of missing out — fuelled a frenzy of investment in infrastructure and chipmakers.

The technology sector's weight in the S&P 500 has climbed above 30%, echoing levels last seen during the dot-com bubble.

Back then, higher interest rates eventually put an end to the party. This time, the bubble has proved more resilient. As the Fed prepares to cut rates next week, investors are left to wonder: which needle will pierce it?

Epilogue

What we now call the "AI bubble" was born not from machine learning breakthroughs but from monetary and fiscal alchemy in 2009 — a blend of cheap money, abundant liquidity and relentless stimulus. AI merely supplied a compelling new story, a promise of epochal change akin to the internet's dawn, giving the bubble fresh energy and legitimacy.

As long as the triple therapy endures, the bubble will keep expanding. The rapid progress of AI feeds daily optimism — and greed. For now, the air keeps flowing in. But every bubble inflates towards the same inevitable end: the pop.

This article is a translation of a column originally published in French on Allnews.ch. Read next: Beneath the Bubble, the Void.

← All publications