Where is the world heading? (And what does it mean for your portfolio?)

The 1990s and 2000s were, in retrospect, unusually kind to investors. Disinflation, globalised growth, abundant liquidity, US leadership: a combination that made asset allocation almost intuitive. That world is gone. What replaced it is harder to read, and the implications for portfolio construction are significant.

The transformations underway — climate change, wars in Europe and the Middle East, the rise of populism, US-China rivalry, tensions over critical resources, the AI revolution — are not isolated shocks. They are structural, interconnected, and they do not resolve on a business cycle. Uncertainty is no longer a phase. It is the regime.

Structuring the unstructurable

Donald Rumsfeld's framework — known knowns, known unknowns, unknown knowns, unknown unknowns — is a useful starting point. It forces intellectual honesty about what we know versus what we merely assume we know. But for investors, it stops short of being actionable.

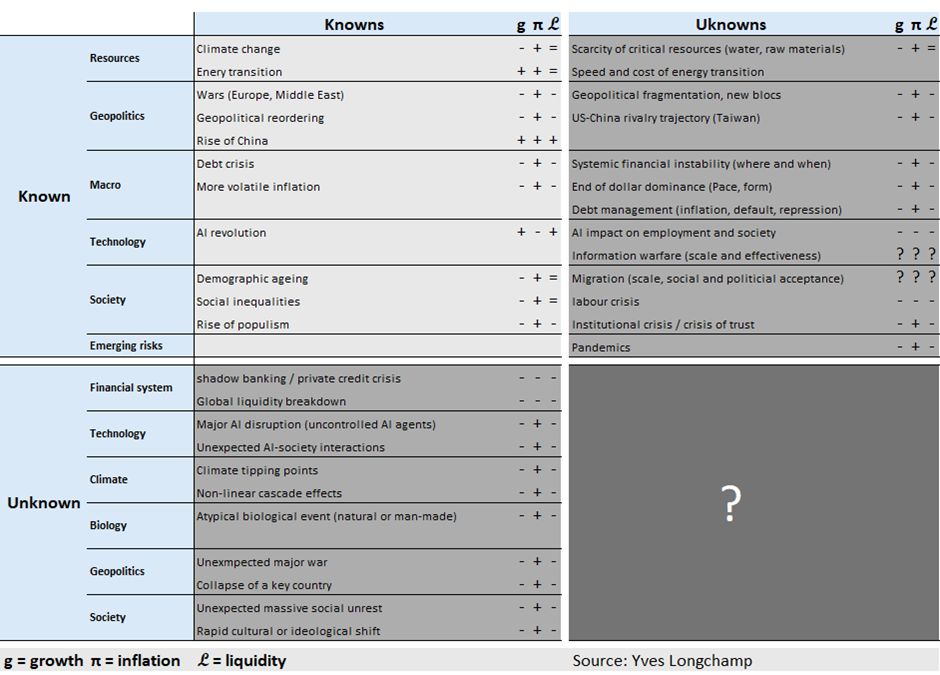

The operational complement is a triad of three variables: growth, inflation and liquidity. These three axes define macroeconomic regimes, and regimes determine asset performance far more than any single forecast. The figure below maps the landscape through this lens.

What it reveals is uncomfortable. The known knowns — already priced by markets — point toward a structurally less favourable backdrop: lower growth, stickier inflation, tighter liquidity. Add the risks with limited visibility (the other quadrants), and the trajectory could be more challenging still.

Growth: the end of easy beta

Global growth is not disappearing, it is dispersing. AI and technological innovation offer genuine productivity upside. But demographic ageing, elevated sovereign debt and economic fragmentation create persistent drag on aggregate potential.

The practical consequence: performance no longer comes from riding a broad wave. It comes from selection — identifying companies with strong balance sheets, genuine pricing power and cash flows that hold under pressure. The dispersion between winners and losers, across sectors and geographies, will be wider than investors have been accustomed to.

Inflation: a structural guest, not a cyclical visitor

Four decades of disinflation trained investors to treat bonds as reliable ballast. That assumption deserves scrutiny. The energy transition, industrial reshoring and resource scarcity are exerting durable upward pressure on costs. Inflation has structural roots now, not merely cyclical ones.

For portfolios, this reframes the role of real assets (energy, commodities, infrastructure) from tactical positions to strategic allocations. It also raises a more granular question at the company level: who genuinely has pricing power, and who is merely passing costs through temporarily?

Long-duration assets remain the most exposed if real rates continue to drift higher.

Liquidity: the variable that turns corrections into crises

Liquidity is consistently underweighted in strategic thinking until it isn't there. Since 2008, it has been a tailwind: central bank accommodation and the structural dominance of the US dollar provided a reliable floor. That floor is less certain today.

Monetary tightening, financial fragmentation and growing stress in shadow banking and private credit markets are making liquidity more conditional. The critical point is this: liquidity is what determines whether a market dislocation stays orderly or cascades. A portfolio that performs well in normal conditions but carries hidden illiquidity pockets is not a resilient portfolio but a fragile one wearing a resilient mask.

Maintaining genuinely liquid buffers and managing leverage with discipline are structural necessities.

Building a portfolio for the regimes, not the forecast

These three axes do not operate independently. It is their interaction, the specific combination of growth momentum, inflationary pressure and liquidity conditions, that defines the market environment at any given moment. And that environment can shift faster than consensus views.

This has a direct implication for allocation. A portfolio built around a single central scenario is a concentrated bet on that scenario being right. The alternative is a portfolio designed to remain functional across several plausible configurations, not by hedging everything into mediocrity, but by avoiding the fragilities that only reveal themselves when conditions deteriorate.

In practice, this means three things.

First, diversification that is tested against stress, not just calm markets. Correlation structures change in adverse conditions, and the diversification that looks robust today can collapse precisely when it is needed most.

Second, deliberate exposure across all three axes: real assets to hedge inflation risk, quality equities to capture growth selectively, and liquid reserves to preserve the capacity to act when dislocations create opportunity.

Third, ongoing attention to implicit concentrations, i.e. exposures that look diversified on the surface but share common underlying drivers. These are among the hardest risks to see and among the most consequential when they surface.

Where is the world heading?

The question "where is the world heading?" does not have a clean answer. The range of plausible outcomes is wider today than it has been for a generation.

But for investors, the more useful question is a different one: is your portfolio built to navigate multiple scenarios, or does it depend on one of them being right?

A portfolio is not a forecast made tangible. It is a navigation instrument and right now, the conditions warrant careful navigation.

This article is a translation of a column originally published in French on Allnews.ch.

← All publications